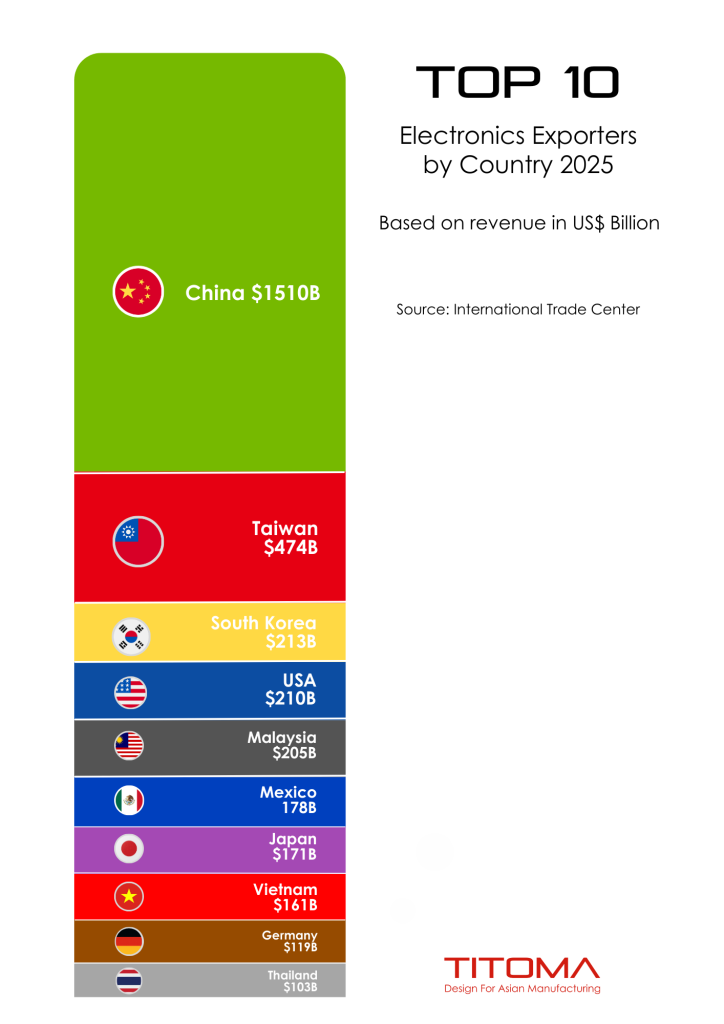

As of the data for 2026, China maintained its position as the world’s largest electronics exporter, holding a 32% share of total global exports with a total value of $1,510 billion. Taiwan secured the second position with a 14% share of high-tech exports; its value surged to a record $474 billion, propelled by an unprecedented global demand for AI-related components and semiconductors.

In contrast, the United States climbed to the sixth position globally, contributing a 5% share of total electronics exports with a total value of $210 billion, reflecting a significant recovery in domestic semiconductor and high-end hardware manufacturing.

TOP 10 ELECTRONICS MANUFACTURERS BY COUNTRY IN 2023-2026

(IN US$ BILLION)

- China $1,510B (32%)

- Taiwan $474B (14%)

- South Korea $213B (8%)

- United States $210B (5%)

- Malaysia $205B (5%)

- Mexico $178B (4%)

- Japan $172B (4%)

- Vietnam $164B (4%)

- Germany $155B (4%)

- Thailand $125B (3%)

GEOPOLITICAL SHIFT RESHAPE SEMICONDUCTOR LANDSCAPE

(As of early 2026, the global semiconductor industry is undergoing a fundamental structural realignment)

According to recent IDC reports, the push for supply chain resilience has moved from theory to reality. The implementation of various national “Chips Acts” has mandated that manufacturers adopt ‘China + 1‘ or ‘Taiwan + 1‘ production strategies. These policy changes are aggressively driving regional development, particularly in the United States and Southeast Asia, to diversify the foundry and assembly/test segments.

Major industry leaders including TSMC, Samsung, and Intel have hit significant milestones in their U.S. based projects over the last 12 months.

• TSMC Arizona: By January 2026, TSMC’s Phoenix facility reached full capacity for 4nm and 5nm production, with yield rates matching its primary facilities in Taiwan.

• Intel Foundry: Intel officially entered high-volume manufacturing for its 18A (1.8nm) process in Arizona in early 2026, marking a historic breakthrough for U.S. logic leadership.

• Samsung Taylor: Samsung has pivoted its Texas operations to focus on 2nm Gate-All-Around (GAA) technology, securing major AI customers for upcoming production cycles.

Meanwhile, China has accelerated its technological self-sufficiency. Beijing is leveraging massive local demand and state guided investment funds such as the “Big Fund” Phase 3 to bypass international trade restrictions. This third phase of funding, totaling over $47 billion, is specifically targeted at eliminating supply chain chokepoints in lithography and advanced packaging.

Industry forecasts from SEMI’s 2027 Equipment Report indicate that the global foundry landscape is becoming more regionalized:

The United States is expected to see its share of advanced processes (7nm and below) jump to 21%.

China is projected to hold 31% of total capacity, focusing on mature nodes.

Taiwan’s share will adjust to 40% as it expands its international footprint.

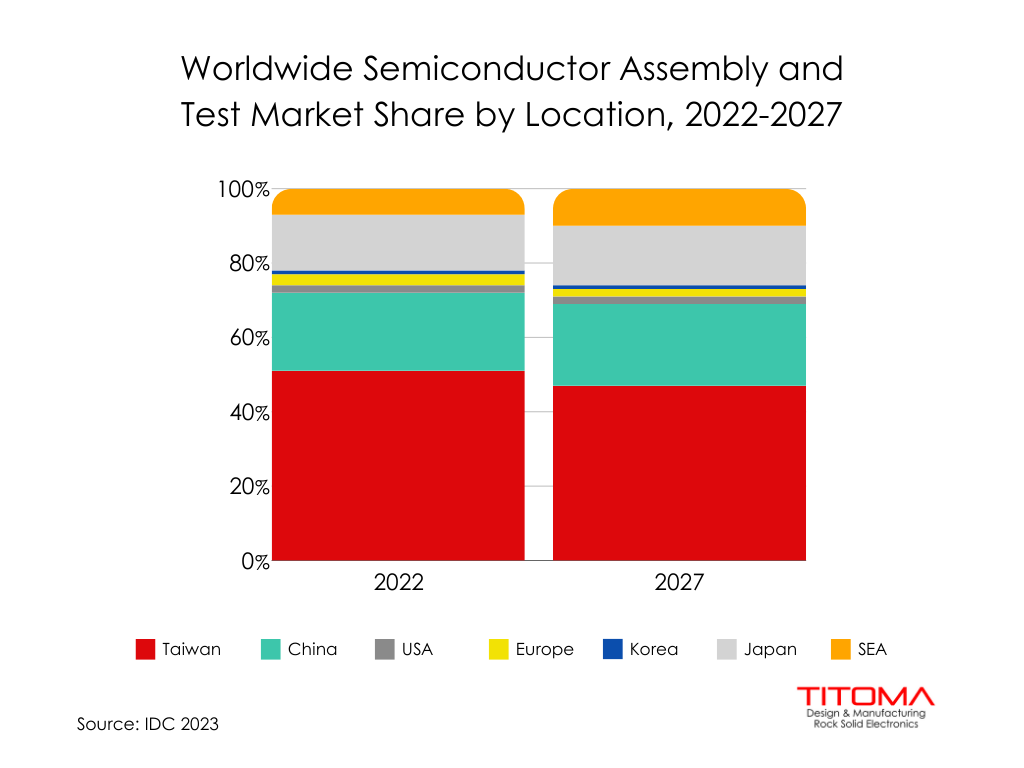

Due to intensifying geopolitics, rapid technological advancements, and high talent availability, major integrated device manufacturers (IDM) from the United States and Europe are significantly increasing their capital expenditures in the Southeast Asian market. Simultaneously, the world’s leading OSAT (outsourced semiconductor assembly and test) companies are aggressively shifting their focus from China to Southeast Asia to de-risk their supply chains.

Consequently, Southeast Asia has solidified its role as a critical pillar in the global semiconductor assembly and test market, with Malaysia and Vietnam emerging as the primary beneficiaries. Recent 2026 data shows that:

• Southeast Asia’s share of the global semiconductor assembly and testing market is now projected to reach 14% by 2027 (surpassing the earlier estimate of 10%).

• Taiwan’s share of the global assembly and testing market is projected to decline from 51% in 2022 to 46% by 2027 as it shifts its domestic focus toward high-margin “Advanced Packaging” (CoWoS) for AI chips, while moving high-volume legacy testing to Southeast Asian hubs.

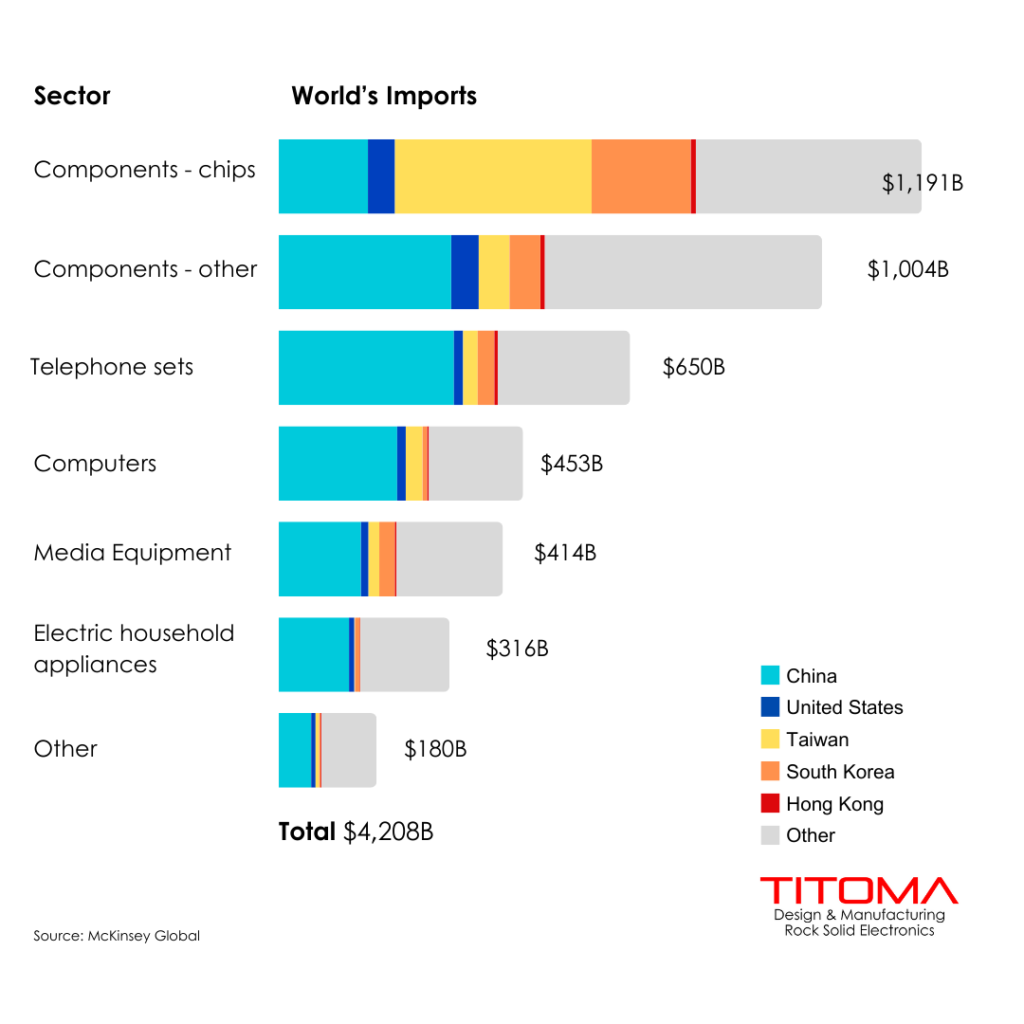

THE WORLD’S ELECTRONICS TRADE WITH ITS TOP 5 TRADING PARTNERS

The below graph shows the composition of imports and exports in electronics in 2022-2023 and the share of the top 5 trading partners of the world. (source: McKinsey Global Institute)

Most imported electronics are component chips, with Taiwan being the largest country from which the world sources them. It is no surprise, given that Taiwan is home to TSMC, the world’s largest semiconductor foundry. Check out more about the Top 10 Biggest Semiconductor Companies here.